*The information contained in this post is not meant to be specific for you or your situation and is not meant to be financial advice, as I am not licensed as a financial planner. Before making any decisions, I strongly recommend speaking to someone licensed in this area to consider your unique situation. My recommendation in this area would be Will Butler.

Disclaimer: From discussions that I have had on this subject in the past, I realize that this is a controversial topic. I have never been one to shy away from discussion on touchy subjects whether ethical or financial in nature. This post will be about the financial side of the decision that I have made.

One of the first posts I ever wrote on this blog was regarding student loan repayment. This was about 10 months ago and it has been the second most popular post that I have written to date. This is not surprising considering the huge amount of outstanding student loan debt faced by many from rising tuition costs. If you have no idea about income based repayment options then it would probably be a good idea to go back and read my original post before you continue for some context. Since I wrote that post, I have continued to ponder the different options and research what is best for me financially in the long run. In the original post I concluded that the Pay As You Earn (PAYE) option was the best option in my situation and likely to be a very good option for others. Since then, I have discovered that there is an even better option available that I had completely dismissed previously.

The income driven repayment plan that I have determined is best for me financially at this point is the Revised Pay As You Earn (REPAYE) plan. This option was first introduced at the end of 2015 and at first glance it didn’t seem very enticing for those with graduate school debt, but upon further investigation, it is likely a very good option for most of us choosing between income driven repayment plans. Under the REPAYE option, your payment is set at 10% of your discretionary income which is the same as PAYE. Forgiveness for undergraduate loans occurs after 20 years, exactly like PAYE, but for graduate school loans, the remaining balance is not forgiven until 25 years of payments. The 25 year forgiveness is the reason that I didn’t initially consider this option fully since all of my loans are graduate loans. However, REPAYE has a very powerful benefit: half of all accumulated interest will be forgiven each month.

This is a huge benefit for those of us with income based payments that are less than our accumulating interest. Under the PAYE plan your balance would grow much more quickly in this situation due to the remaining interest being capitalized (added to the principle balance) at the end of each month. Let’s look at some easy example numbers to demonstrate this. If you have $100,000 in loan balance and your average interest rate is 10% and your monthly payment is $0/month based on your income, you would be accumulating $833.33 per month in interest that would be added directly onto your principle balance based on the PAYE plan. With REPAYE, this accumulated interest is cut in half and only $416.67/month would be added to your balance. The benefit will change based on your loan terms and your monthly payment, but for some this will be a blessing.

In this post I’m going to compare three different options for repayment, those being: Standard 10 year repayment, PAYE, and REPAYE. I’ll use the numbers for my personal situation and then also the numbers for a more average new grad who is taking a regular full time job. The reason my situation is different than many others is due to the tax free stipends involved in travel physical therapy. Because of these stipends, my adjusted gross income (how income based payments are determined) is not as high as it would be if I was working a full time permanent job.

Before I get to the numbers, I want to bring up some of the points from my last post that still apply.

- There is a tax deduction based on the amount of interest you pay on your student loans up to $2,500 per year, even if you don’t itemize your return. This deduction is phased out if your AGI is above $80,000, but I don’t think that will ever happen for me based on 401k contributions reducing my AGI. You do not receive that full $2,500 back on your taxes, but will receive some percentage of it based on your income, likely somewhere in the neighborhood of 20%-25%. That means somewhere around $600 being returned to you each year on your taxes. $600 x 20 years = $12,000. If you choose the standard 10 year repayment, you total deduction will be less than half of that, due to paying less interest the last few years as your principle balance decreases.

- There has been legislation proposed to no longer have the forgiven loan balance count as unearned income (meaning that you have to pay taxes on what’s forgiven), which would make loan forgiveness a much better option. There is no way to know if this will ever go through, but I would imagine there is at least a small chance over the next 20 years.

- Investing the difference between what you would have spent on the standard 10 year repayment plan and your payment on an income based repayment plan can serve as a life insurance policy of sorts. The reason for this is that student loan debt is discharged upon death. Imagine that you put all of your money toward your loans and then pass away at the end of the 10 year repayment period. You wouldn’t have any assets to leave to your loved ones. On the other hand, imagine that you choose an income driven repayment option and invest your extra money and then pass away after 10 years. The remainder of the loans will be forgiven and all of your investments can be passed on to your heirs. This may not be a game changer for many but it is something to consider.

Alright, so all of the considerations above should make one lean in favor of an income based repayment plan, but let’s look at the numbers, first for someone in a situation like mine with a lower adjusted gross income ($50,000) and a starting loan balance of $97,000 at 6% interest:

Under both PAYE and REPAYE, monthly payments would be $218 (10% of discretionary income). For standard 10 year repayment, the payment would be $1077/month.

REPAYE: ~$112,000 paid total over a 25 year period. This includes $65,400 paid in monthly payments $218 * 12 * 25 = $65,400. At the end of the 25 year period a balance of $155,400 would be forgiven. Assuming a 30% tax rate on this forgiven amount, $155,400 *.3 = $46,620. This leads to the total amount paid, $65,400 + $46,620 = $112,020.

PAYE: ~$116,800 paid total over a 20 year period. This includes $52,320 paid in monthly payments $218 * 12 * 20 = $52,320. At the end of the 20 year period a balance of $214,900 would be forgiven. Assuming a 30% tax rate on this forgiven amount, $214,900 * .3 = $64,470. This leads to the total amount paid, $52,320 + $64,470 = $116,790

Standard 10 year repayment: ~$129,000 paid total over a 10 year period. $1,077 * 12 * 10 = $129,240.

In this scenario REPAYE is clearly the winner with PAYE in second and standard repayment in last place.

Now let’s look at a scenario with the same interest rate and loan balance but with an AGI of $70,000:

Under both PAYE and REPAYE, monthly payments would be $435 (10% of discretionary income). For standard 10 year repayment, the payment would be $1077/month.

REPAYE: ~$162,900 paid total over a 25 year period. This includes $130,500 paid in monthly payments $435 * 12 * 25 = $130,500. At the end of the 25 year period a balance of $107,900 would be forgiven. Assuming a 30% tax rate on this forgiven amount, $107,900 *.3 = $32,370. This leads to the total amount paid, $130,500 + $32,370 = $162,870.

PAYE: ~$140,100 paid total over a 20 year period. This includes $104,400 paid in monthly payments $435 * 12 * 20 = $104,400. At the end of the 20 year period a balance of $119,100 would be forgiven. Assuming a 30% tax rate on this forgiven amount, $119,100 * .3 = $35,730. This leads to the total amount paid, $104,400 + $35,730 = $140,130

Standard 10 year repayment: ~$129,000 paid total over a 10 year period. $1,077 * 12 * 10 = $129,240.

Uh oh, in this scenario we can see the impact that the extra five years of repayment has when the accumulating interest is less each month due to a higher monthly payment. This puts REPAYE in last, PAYE second, and standard 10 year repayment first. But not so fast, there is a very important factor that is not being accounted for here.

Monthly payments under any income based repayment plan are based on your adjusted gross income. Your adjusted gross income is reduced with eligible deductions such as 401k contributions ($18,000 maximum per year), traditional IRA contributions ($5,500 maximum per year) and HSA contributions ($3,350 maximum per year). This means that making smart decisions for your retirement will not only help you later in life but also will decrease your AGI and therefore your total amount paid on your loans when using an income driven repayment plan.

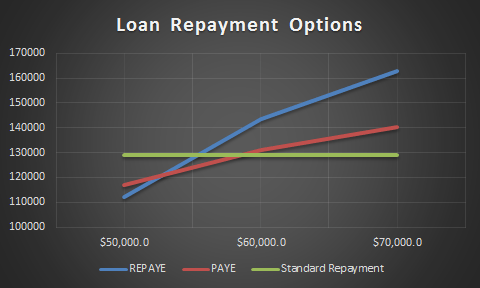

So if $70,000/year AGI leads to paying more overall when using an income driven repayment plan and $50,000/year AGI leads to a lower overall amount paid, you may be wondering where the cut off values are for this scenario. Well, I spent a long time trying to figure out how to display this in a graph (I’m not great with Excel) and here is what I came up with:

The Y axis is the total amount paid over the life of the loan. The X axis is yearly AGI. Keep in mind that these numbers are based on $97,000 in direct subsidized loans with an average interest rate of 6%.

Based on the graph for this scenario, if your AGI is below ~$52,500 you come out ahead with REPAYE. If it’s between ~$52,500 and ~$58,000 then PAYE is the best choice and if your AGI is above $58,000 then the standard 10 year repayment is the best option. That seems simple enough, but the total amount paid doesn’t tell the whole story. The reason for this is that with PAYE that amount is paid over 25 years, with PAYE it’s paid over 20 years and with the standard repayment it is paid over 10 years. In that 15 year period between the standard repayment finish date and the REPAYE finish date, the value of money will generally decrease by quite a bit. Historically, the dollar loses 35% of it’s spending power in an average 15 year period due to inflation. Trying to factor inflation into each payment over the 25 year period is way above my level of Excel prowess, but it would likely push these cut off numbers to the right by a decent amount making the argument for income driven repayment even better.

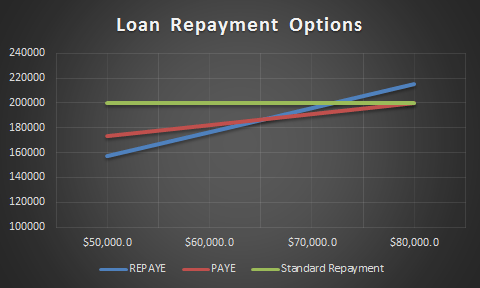

Now I’ve talked to a lot of other new grad physical therapists over the years and it seems that, unfortunately, $100,000 in student loans is on the low end of the spectrum. For that reason I made a graph for those with $150,000 in student loans at an average interest rate of 6% to see what the difference would be:

On this graph we can see where income driven repayment plans really shine. As total student loan debt increases, the argument for income based plan repayment plans becomes much better. If you have $150,000 in student loan debt at an average interest rate of 6%, you would have to have an AGI of well over $80,000 (factoring in inflation) in order to come out ahead by using the standard repayment option. Although the numbers are interesting to see, it shouldn’t come as a surprise that having high student loan debt makes income driven repayment a better option because these are the exact people for which these plans were made.

Alright so let’s try to wrap this all up and come to some sort of a conclusion.

From the very beginning of your career, you should be contributing a decent amount (likely 10-15% or more) of your income to tax advantaged accounts (401k, traditional IRA, HSA). This will not only allow you much more freedom later in life but also reduce your student loan payment and total amount paid under an income driven repayment plan. Putting $10,000 per year into a combination of a 401k and HSA can lead to a significant reduction in your AGI, which not only spares you in taxes at the end of the year but also reduces the total amount paid over the life of your loans ($20,000+ in some of the scenarios above). The higher your student loan balance, the more likely that an income driven repayment plan is the best option for you. The lower your AGI, the more likely an income driven repayment plan is the best option for you. Inflation has a significant impact on money over time, so paying $100,000 over a 25 year period is far from the same as paying $100,000 over a 10 year period. Tax deductions for payments made on student loan interest can lead to significant savings over a 20-25 year period which makes income driven repayment plans even more compelling. The tax rate I used for the forgiven balances in the examples above was 30%, but this will be different based on your situation. Personal preference should be a factor in your decision. I have talked to some people that are extremely debt adverse and although they may come out ahead with an income based option, it isn’t worth the psychological stress carrying the debt would cause for them over such a long time.

One last thing to note is that I did not account for any sort of yearly increase in pay in the calculations above. There are three reasons for this: first, because it is impossible to generalize a standard increase in pay because everyone’s career will be different. Second, because I have spoken to very few physical therapists that have worked 25 straight years full time. Most seem to transition to PRN or part time as they advance in their careers which will obviously mean a lower AGI later on, not higher. Third, because as your pay increases throughout your career, you should strive to keep expenses close to the same level and contribute the difference to tax advantaged investment accounts which would keep your AGI, and therefore your payments, at the same level.

I know this is a lengthy post, but this is not a simple topic. I get a lot of questions regarding student loans and I want this to be a resource for new grads that are lost. What is your opinion of standard repayment vs. income based repayment? I’d love to hear your thoughts in the comments.

Great Article! I am curious if you have heard anything about loan forgiveness programs (either good/or bad). I was talking with a guy the other day who has >250k in debt from PT school. He has several children and works for a non-profit employer in Az. He has elected to participate in a 10 year repayment which is income based, which results in him only paying ~300ish dollars a month. He stated at the end of 10 years all loans are forgiven meaning he will only end up paying ~ (300×12= 3600; 3600 x 10= 36,000) 36k while ~214k will be completely gone. He has been doing this for several years so far apparently in his words “paying the amount similar to a car payment while some of my previous classmates are paying basically a second mortgage”.

LikeLiked by 1 person

Justin, you’re talking about the public service loan forgiveness program (PSLF). This is by far the best option for most if they’re eligible (work as a government or nonprofit job). The PSLF plan is sewerage from the income based repayment plans meaning that you would pick one of the income based plan to start with, work at a non profit or government job for 10 years while making your payment under the income based plan you choose, and then have the remainder of your loans forgiven at the end of that 10 year period. The reason this leads to the lowest amount paid is that you get to skip either 10 or 15 years of payments, depending on the income based plan you choose, as well as pay no taxes on the forgiven amount like you would under normal 20-25 year loan forgiveness. I’d say the guy you were talking to has a very good plan for his situation.

LikeLike

Great post! I am a new grad nurse working for a non profit and am interested in pursuing PSLF. My payments under REPAYE are $170 and my total loans are $33,000. I make about $56,000 gross (before pre tax contributions). I’m curious what your thoughts are for those of us with (relatively) low loan balances. From my calculations I could have about $15,000 forgiven after 10 years but I’m unsure if paying them off early would be the better route. Love to know your thoughts and keep up the good work on the blog!

LikeLiked by 1 person

Thanks, Amanda. If you’re going to be making about the same amount of money at a nonprofit hospital as you would somewhere else and you like your job, I don’t see any reason not to go for PSLF. Even if the savings aren’t anything huge, I’d go with REPAYE or PAYE, invest the extra money in pretax accounts to further reduce your payments, and then get the PSLF in 10 years!

LikeLike

Thanks so much for your reply!

LikeLiked by 2 people

Hi there,

One thing I think you should mention is the impact on marriage on IBR plans. On PAYE, you can marry filed separately and your spouse’s finances don’t count towards your AGI. On REPAYE, no matter which way you file, their finances are added to yours as your total AGI. In my case, my SO currently makes 90k. If we get married, I’d be paying so much more in loans. I can’t imagine the tax advantage of married filing jointly could ever make up for that difference.

Thanks!

LikeLiked by 2 people

That’s a very good point, Erin! There are a lot of intricacies in the different repayment plans which is frustrating when attempting to plan for the future. One good thing is that you can freely switch between plans right now while having the prior payments still count toward forgiveness. That means that someone could use REPAYE right now if it makes sense for them to do so and then change to PAYE if the situation changes such as with marriage.

LikeLiked by 1 person

So if I use REPAYE for 10 years, get married, and opt to switch to PAYE, I:

a) get interest slashing benefits of REPAYE for first 10 years

b) get the benefit of forgiveness @ 20 years with PAYE rather than 25 years with REPAYE

This has to be too good to be true..what am I missing?

LikeLiked by 1 person

As of right now this is exactly how it works although it could definitely change in the future. The only downside of changing plans in that scenario would be that the interest that accrued while on REPAYE (not the interest that was subsidized each month) will be capitalized meaning interest will start accruing on that interest. It’s my understanding that while on REPAYE the interest accumulates but doesn’t actually capitalize so you wouldn’t pay interest on that interest until you change plans. Not a huge deal at all for the benefits, especially with a low taxable income, but something to consider.

This is very similar to my plan right now unless things change.

LikeLike

Hi Jared,

Amazing post and thank you for sharing. The way I’m seeing this, it almost seems like no matter the amount of student loans you have, REPAYE is the best option given that interest will only accumulate at 3% over 25 years and all that time you could be investing money in what would otherwise be going into your loans into index funds instead, which of course would likely accrue greater than 3%. Am I overlooking something or do you see it that way as well? If you’re looking to invest as much as possible early on, is there any scenario where REPAYE would not make sense? I have a relatively low (~35k) amount of student loans so I don’t fit so perfectly into the case you’ve made for REPAYE. Thanks!!

LikeLiked by 1 person

Thanks for reading, Lucas! In my analysis, I think the times it wouldn’t make sense to go on REPAYE are when income is high enough or will be high enough in the future to make payments so high that the remaining balance will be very low or completely gone at the end of the 25 years. There’s also some complication with REPAYE and marriage where depending on how much a future partner makes that could make it not the best choice. The best part with those things though is that if it ever doesn’t make sense then it’s free to switch between plans. As a single individual with a low AGI, I haven’t seen a compelling reason to go any other way with repayment though.

LikeLike

What do you think if you have a low AGI, but also a low total amount of loans, so that the balance will likely be gone at the end of 25 years? Could you possibly share your excel sheet if you still have it? I’m having a hard time wrapping my head around this math and if there’s any benefit to REPAYE if your payments will likely be larger than accumulating interest, negating the advantage of the accumulated interest subsidy. Thanks again, Jared!

LikeLike

If the payment is likely to be higher than the accumulating interest and the payment is high enough that there won’t be a remaining amount after 25 years, then there isn’t a benefit to REPAYE. In that case I would refinance to get the lowest rate possible and pay the debt off as quickly as I could!

LikeLike

I’m currently on PAYE but haven’t made a single payment due to my grace period (graduated Dec 2019) and then COVID forbearance. My AGI the last few years has been $60-$70k but I will be going into travel therapy and plan to lower it to ~$18,809 as you mentioned in your articles.

I do plan to get married by 2025 (increasing AGI by $60-80k, they are not a traveler). Would it be worth it to switch to REPAYE for a couple of years before switching back to PAYE after marriage? Or should I leave it alone?

LikeLiked by 1 person

I’d wait for now. There’s a new repayment plan being proposed that would be 20 years to forgiveness and no interest would be accrued at all even with a $0 monthly payment. If that goes through then it will be better than PAYE or REPAYE, especially for travelers with a low AGI. If for some reason it isn’t implemented then I’d probably go on REPAYE until you get married and then recalculate then to see if it still makes sense based on the new income. It’s pretty easy to switch back and forth and payments carry over.

LikeLike