Travel Therapy and Improving Your Finances

Hello again. If you’ve read any of my posts in the past then you probably already know that I enjoy writing about a lot of things, but two at the top of my list of favorites are travel therapy and personal finance.

Today I want to make a case for the financial superiority of travel therapy as a new grad and use some numbers to illustrate my point. I think most people realize that you can make quite a bit more money as a travel therapist, and I’ve written about this in the past (I also wrote a post for NewGradPT regarding student loan repayment with travel therapy here), but I don’t think that most therapists realize how powerful compounding interest can be early in your career.

What is Compounding Interest?

By definition (source: Wikipedia): Compound interest is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. It is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest.

Compounding interest is something that is very difficult for us to comprehend intuitively, which has led to many people being fascinated by the idea, including Albert Einstein himself.

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

“Compound interest is the most powerful force in the universe.”

“Compound interest is the greatest mathematical discovery of all time.”

-Albert Einstein

The fact that he has multiple quotes regarding the power of compounding interest should pique your curiosity.

Example Scenario: The Basics

Let’s compare a couple different scenarios to see the power of compounding at work. Since I’ve written about paying off debt with travel therapy in the past, I’ll focus on taking advantage of investing in a well diversified index fund portfolio.

- Steve is a new grad physical therapist. He graduates and takes a permanent job in an outpatient clinic with a starting salary of $68,000/year.

- Steve has yearly expenses of $40,000 (including his minimum student loan payment on a standard 10-year repayment plan). The remaining money he saves and invests in a brokerage account to take advantage of compounding interest

- Mark is a new grad physical therapist. He graduates and decides that he would like to work as a travel therapist for three years to earn extra money, explore the country, and decide where he wants to live before settling down. Over his three years as a traveling therapist, he makes an average of $1,700/week AFTER taxes. This may seem like a lot of money, and it is, but this is definitely possible, especially on the west coast, and is a number that is close to what Whitney and I have averaged since graduating and traveling as new grad PTs.

- Mark has higher expenses than Steve since he has to pay for housing expenses in two locations, at his tax home and at his travel assignments (a requirement to receive tax free stipends). He decides to rent a room in his hometown that he can return to between assignments which will serve as his tax home where he pays $400/month. He also pays more for housing at his travel assignments since short term housing is more expensive. His total yearly expenses come to $50,000. (This includes his monthly student loan payments on a standard 10-year repayment plan, just like Steve’s.) The extra $10,000 in his expenses compared to Steve’s is due to extra costs incurred while traveling.

Steve receives generous benefits at his permanent job and gets four weeks of vacation per year! Mark also takes four weeks off per year to go back to his tax home between assignments, but is unpaid during that time. Both receive health insurance coverage through their employers with the same out of pocket premium costs which is factored into their expenses below. Now, we know what Mark’s weekly after tax income is and from there we can figure out his monthly income and use his yearly expenses to find his monthly expenses. We can do the same for Steve by determining his after tax income based on his yearly salary using PayCheckCity.

- Mark:

- Income: $1,700/week * 48 weeks / 12 months = $6,800/month after taxes

- Expenses: $50,000 / 12 months = $4,167/month

- Surplus: $6,800 – $4,167 = $2,633/month * 12 months = $31,600/year

- Steve:

- Income: $68,000/year salary equates to yearly after tax pay of $50,000. $50,000 / 12 month = $4,167/month after taxes. This is based on Steve living in and paying Virginia state taxes.

- Expenses: $40,000 / 12 months = $3,333/month

- Surplus: $4,167 – $3,333 = $834/month * 12 months = $10,000/year

I chose to express all of these values in both monthly and yearly terms so that you can easily compare to your own situation.

Example Scenario: The Investment Potential

So far we see exactly what I, and probably you, expected to see. Travel PTs, even including unpaid time off and additional expenses, come out significantly ahead financially. This has certainly been the case for Whitney and I and is what has allowed me to “semi-retire” this year at 29 years old after working for only three years. What we can’t see here is how that surplus, when invested properly, will grow over time.

Let me enlist the help of my rudimentary excel skills to look at what happens to those amounts if you take the surplus and invest it over a three year period.

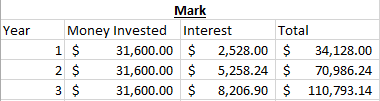

Here is our first glimpse into the power of compounding interest. Steve and Mark both had their money growing at a yearly interest rate of 8%. Over a three year period, Mark ends up with over $75,000 more than Steve even though he only invested about $65,000 more than Steve.

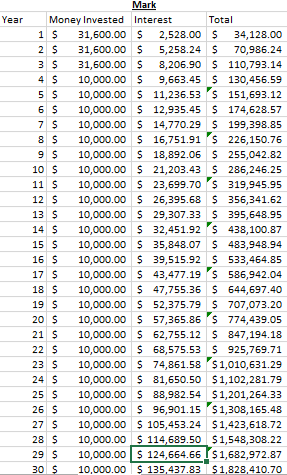

Now lets assume that after three years of traveling Mark settles down and takes a full time job. He also decides to work at an outpatient clinic with the same yearly salary as Steve, $68,000/year. Now that he has settled down and doesn’t have to maintain two separate residences or pay higher costs for short term housing, his expenses drop to the exact same amount as Steve’s, $40,000/year. That means that from year four on, both Steve and Mark will be saving the exact same amount, $10,000/year, the only difference is that at year four Steve has $35,000 in his investment account while Mark has $110,000 since he decided to travel as a new grad and save the extra money he made. Let’s look at what this looks like after a 30 year career when both of them are considering retirement.

Steve ends up with an impressive $1,223,000 amount in his investment accounts! This isn’t even considering any matching from his employer that he would, hopefully, receive over the years if he chose to invest in his 401k. But what about Mark, how much did that extra savings from travel mean for him at the end of his career?

Mark ends up with $1,828,000 after 30 years! That’s over $600,000 more than Steve even though he only actually invested $65,000 more than Steve at the beginning of their careers, and they earned the same interest rate on their money each year! How astounding is that? This is also not assuming any 401k matching through his employers, if he chose to invest in this account over the years, which would likely push him over $2,000,000! This shows the awesome power of compounding interest and would make even Mr. Einstein proud.

Summary of the Financial Benefits of Travel Therapy

So after looking at this example, it is clear that travel therapy early in your career can make a massive difference in your long term financial situation. It also shows how saving early in your career is vital for having compound interest work in your favor, even if you don’t decide to travel. In Steve’s example, he saves only $300,000 total throughout his career, but because of compounding ends up with over $1.2 million. Had he waited to start investing until 10 years later, you can bet that his situation wouldn’t be as good, even if he invested that same $300,000.

So Does That Mean Travel Therapy as a New Grad is Right For You?

I anticipate that there will be some objections to traveling as a new grad as I’ve written about this in the past and have heard from many people who believe that this is not a good idea. I was even advised against it while in school, but I couldn’t be any happier with my choice. You can read through some of my older posts on traveling as a new grad (here, here, and here) for more information on my opinion, but I’ll summarize some of it here.

- Travel therapy as a new grad is only for you if you feel confident in your evaluation and treatment skills when coming out of your last clinical. If you still feel uncertain, then having a permanent job for a while to learn and build you confidence may be a good idea.

- Make sure to be picky on your first couple of travel assignments and start with the setting that you’re most comfortable in and at a facility that sounds good during the interview.

- Most travel companies offer a “clinical mentor” that you can contact if you have questions about anything related to your practice. Take advantage of this mentor for situations that you are unfamiliar with and also use online groups and blogs to learn and receive advice.

- A common objection revolves around not developing as a clinician due to not having an in person mentor while traveling as a new grad. I think that this is not true if you take advantage of other clinicians at each facility, continuing education opportunities, as well as online resources. Not only can you develop your skills well as a new grad traveler, but you’ll be a more well rounded clinician if you allow yourself to branch out and try many different settings.

Helping You Get Started

If travel therapy sounds like something that you’re interested in, new grad or experienced clinician, but you don’t know where to start, reach out to me or Whitney! We have helped and mentored over 100 new travelers at this point and are always willing to help however we can. Start with some of the posts that I linked to above and then send one of us a Facebook message or email with questions or for suggestions on the best recruiters/travel companies.

Travel therapy early in your career is a wonderful opportunity to set yourself up for a rock solid financial situation later in life. In addition to the financial benefit, travel therapy gives you a great opportunity to experience different settings and different parts of the country. If travel therapy is feasible for you life situation, give it a shot! Worst case scenario, if you don’t enjoy it, you work for three months and then go back home to a permanent job. Good luck with whatever you decide to do in your career!

*Clarifications for the example presented:

- In both examples I assume that the raises they get each year keep pace with inflation, which is why the amount saved stays the same each year for both of them.

- I strongly encourage everyone to take advantage of pretax accounts during working years to reduce tax burden while income is high.

- Since I’m using all after tax numbers in the example above for simplicity, these calculations aren’t taking into account additional tax savings that could be achieved by using pretax accounts for both of them.

- Maximum contribution limits for pretax accounts are currently (as of 2018):

- $18,500 for 401k

- $5,500 for Traditional IRA

- $3,450 for HSA

Thanks for reading!

2 thoughts on “A Case for Travel Therapy as a New Grad: The Power of Compounding Interest”