*The information contained in this post is not meant to be specific for you or your situation and is not meant to be financial advice, as I am not licensed as a financial planner. Before making any decisions, I strongly recommend speaking to someone licensed in this area to consider your unique situation. My recommendation in this area would be Will Butler.*

In my last post I talked about the difference between a Traditional and a Roth IRA and factors you should consider when deciding which account is best for you. That was my first 2,000+ word post, and since it was getting pretty long, I didn’t have room to add in an example comparing the two accounts. If you haven’t read that post yet, I encourage you to so that you have some context on the factors I’ll present in this post. I think using a real world scenario with two people in the exact same financial situation and the only difference being which account they choose should help to shed some additional light on the differences. There are so many different details in each individuals financial situations that will change things, so in order to avoid as much of that as possible, I’m going to do my best to look at an average situation for a single individual to avoid making this comparison more difficult than it needs to be. Keep in mind that just because this is a single person and your situation may be different, the majority of the considerations should still apply to your situation, but the numbers will be different.

The Subjects

Bill and Jim are identical twins. Everything about their lives are exactly the same including: age, job, income, expenses, family situation (single with no kids), and retirement age. Let’s look at the specifics for them:

- Living in Texas with no state income taxes

- Standard deduction on taxes each year

- Income: $52,000/year gross ($41,975/year net after federal taxes and FICA taxes)

- Expenses: $38,975/year after taxes

- Age: 28

- Anticipated retirement age: 60

The employer that Bill and Jim work for does not offer a 401k, so they have to create their own individual retirement account (IRA). Bill decides that he wants to invest for his retirement in a Roth IRA, while Jim decides that he believes a Traditional IRA would be better. Bill invests $3,000/year (the difference between his income and expenses after taxes) into his Roth IRA. He knows that he will pay taxes on his contributions now but will get to withdrawal his contributions and earnings later without taxes. Since Bill and Jim are both in the 25% marginal federal income tax rate while working, Jim is able to contribute $4,000 to his traditional IRA due to not having to pay the 25% upfront tax on the $4,000 that resulted in Bill only having $3,000 to invest per year. Jim understands that he is getting a tax break on his contributions right now but that he will have to pay taxes on his contributions and earnings in retirement when he withdrawals the money.

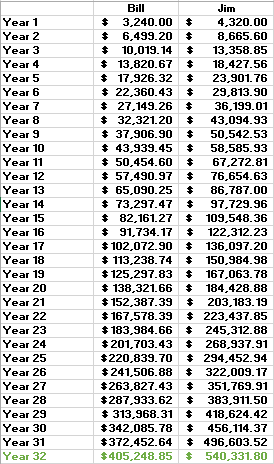

They each contribute the same amount each year (Bill- $3,000 and Jim- $4,000) for 32 years until they reach age 60 and are ready to retire. For the sake of simplicity, lets assume that their income and expenses both remain the same throughout their working careers. Since their financial situations are identical besides the retirement accounts chosen, most of the inflation related increase would negate each other anyway and wouldn’t have a meaningful impact on the example. They each invest their funds inside their IRA’s in a mixture of stocks and bonds that results in a 8% return each year. Let’s check out how their accounts grow over the 32 year period.

As you can see here, Jim ends up with a much larger ending balance, despite investment returns being the same, which is to be expected since he had the advantage of an additional $1,000/year invested due to his contributions being tax free. He also was able to experience compounding interest over the 32 year period on the additional $1,000/year. That leads to a total of $135,000 difference between the two at retirement.

A Closer Look at the Taxes

Now you’re probably thinking, of course Jim has a higher balance at retirement but that doesn’t matter because now he has to pay the piper and is taxed on all of his withdrawals from this point forward, while Bill gets to withdraw from his account tax free. You’re right, from this point on, Bill will be able to withdraw $38,975/year tax free to support his living expenses. So let’s look at exactly how much Jim will have to pay in taxes in order to be able to support his continuing $38,975/year of expenses. This is where marginal vs. effective tax rates come into play which I spoke about in the previous post. While working, when Jim contributed to his Traditional IRA while in the 25% marginal tax bracket, he saved that full 25% since each dollar he contributed was subtracted off the top of his total income which landed in the 25% bracket. This is not the case in retirement since any withdrawals have to fill up the lower tax brackets first before ever making it to the 25% bracket. Here are the current tax brackets with standard deduction and personal exemption to illustrate this point.

As you can see, Bill and Jim making $52,000/year puts them solidly in the 25% marginal tax bracket while working. When Jim subtracts $4,000 from his taxable income by contributing to his Traditional IRA while working, his taxable income goes from $52,000 to $48,000. Since that entire amount is in the 25% bracket, he saves exactly 25% in taxes on that $4,000.

Now we know the marginal tax rate they are in, but what is their effective federal tax rate while working? To figure this out, first we would take their gross income ($52,000) then subtract the standard deduction and personal exemption ($52,000 – $6,350 – $4,050 = $41,600). From there we use the info from the chart above to determine their total tax burden for the effective rate of the 25% tax bracket which is: $5,226.25 + (.25*($41,600-37,950)) = $6,138.75. Now that we know that the total tax burden for them while making $52,000 is $6,138.75, we can determine the effective federal tax rate by dividing the tax owed by the total income earned: $6138.75/$52,000 = 11.8% effective tax rate. This is a lot less than the marginal rate of 25% and why it’s so important to understand the difference.

Withdrawals in Retirement

As I stated earlier, Bill will be able to withdraw the exact amount he needs to live on during retirement which is $38,975 since he doesn’t have to worry about being taxed on his withdrawal. Jim’s situation is a little more complicated since he also needs $38,975 but he needs that amount after paying federal taxes which means he’ll actually have withdraw more than that each year to account for the tax bill. Exactly how much more you ask? It turns out he would need to withdraw $43,470 each year to have $38,975 after taxes. Let’s go through the calculation to see how I got this number using the total tax due calculations from above. Let’s take his gross income ($43,470) in this situation then subtract the standard deduction and personal exemption ($43,470 – $6,350 – $4,050 = $33,070). You’ll notice that since Jim only has to withdraw enough to cover his living expenses from this point forward instead of being taxed on his old $52,000/year income, this drops him down into the 15% effective tax rate after the standard deduction and personal exemption are accounted for. From there we use the info from the chart above to determine his total tax burden for the effective rate of the 15% tax bracket which is: $932.50 + (.15*($33,070-$9,325)) = $4,494.25. Now we take his gross income and subtract his federal taxes due: $43,470 – $4,494.25 = $38,975.75.

This reduces Jim’s effective tax rate in retirement to: $4,494.25/$43,470 = 10.3%! Jim is paying much less in taxes after retirement on his withdrawals than the 25% marginal tax savings he got in the beginning with his contributions. Let’s see how this plays out over the life of his retirement compared to his brother Bill assuming they continue to earn 8% on their investments throughout retirement while Bill withdraws $38,975/year to pay for his expenses and while Jim withdraws $43,470/year which after taxes equals $38,975 to pay for his expenses.

Conclusion

As you can see, Bill only makes it 19 years into retirement before he runs out of money while Jim can continue to support his current expenses for 32 years! That’s a 13 year difference in retirement with the only difference being that Bill chose a Roth IRA and Jim chose a Traditional IRA. I hope that this illustrates not only how, for the majority of people, a Traditional IRA is likely the better option but also how big of a difference even small adjustments to your finances can make over a lifetime. Bill had no idea his retirement would be cut short by 13 years when he made that simple choice at 28 years of age.

There are a few things to keep in mind from this example.

- This is not including social security benefits that they may get in the future. Social security benefits would increase Jim’s effective tax rate in retirement but no where near the 25% marginal tax rate he was able to defer when making the contributions to his Traditional IRA.

- Jim and Bill would likely receive raises throughout their career pushing them into the upper range of the 25% tax bracket and likely even the 28% tax bracket by the end of their career which would further improve the case for the Traditional IRA but the calculations would be much more difficult accounts for promotions and raises.

- Jim and Bill would both have increased expenses throughout their lifetime due to inflation but if the tax brackets also increase with inflation, which makes sense, then these two should balance each other out as far as effective tax rate on withdrawals in retirement is concerned.

- Although Jim and Bill were single throughout their lives, the same math would apply for two similar families trying to decide between a Traditional and a Roth IRA just with different tax brackets, two standard deductions, and more personal exemptions.

What do you guys think? Does a real world example with the calculations make the differences between the accounts easier to see? When considering marginal versus effective tax rates and tax deferred compounding, what scenario can you think of where a Roth would actually come out ahead? The primary factor that most financial advisors site as the reason to choose a Roth over a Traditional is the possibility of increased taxes in the future, but is it worth it to bank on an increase and pass up such a powerful difference as illustrated here?

Hey Jared, thanks for the post. Will you switch to a Roth IRA for years when you take time between contracts and your AGI is lower than the above example?

As you noted in other posts, you’re able to reduce you AGI to the point of paying very little if any taxes by contributing to your 401k and/or HSA. At that point wouldn’t a Roth IRA be preferable?

LikeLiked by 1 person

Hey, thanks for reading! I’m actually still a little on the fence with this but will probably contribute to a Roth in years where my AGI would be less than the standard deduction amount but probably not if it puts me into the 10% bracket. The reason I say probably is because I actually see more benefit to having the money in a standard brokerage account than in a Roth right now with current tax laws but the tax laws could change in the future so I’d like to hedge my bets a little. In a brokerage account right now, I can harvest long term capital gains and qualified dividends for free while in the bottom two tax brackets and harvest capital losses if the market is down (like my international holdings this year) so it’s possible to get the benefits of a Roth (tax free long term capital gains) while having the additional benefit of being able to harvest the losses in down years. I think the ability to harvest the loses combined with more accessibility to the funds in a brokerage account over a Roth more than offsets taxes I’ll have to pay on non-qualified dividends which should be minimal. If the law changes in the future and makes all long term gains and qualified dividends taxed at a flat rate regardless of income level then a Roth would be the better choice in that case offer the brokerage account so I want some money in each. If everything stays the same with taxes, I don’t think there is any income level where a Roth is better than a brokerage account (low income) or a traditional (high income) but the uncertainty of the future makes me want to hedge my bets for sure. Great question!

LikeLike